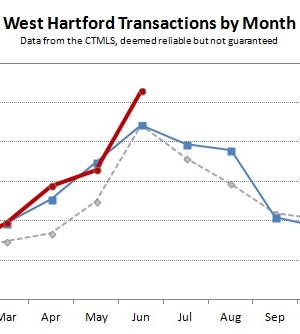

The West Hartford single-family real estate market continues to outperform 2012 in a year-over-year comparison. Closings in June jumped up to 106, which was the best individual month for the town since June 2006 (with 114 closings). Many buyers like to close on their new homes in the summer months. June is usually the peak for closings, with July and August showing modest declines from a June peak depending on the overall strength of the

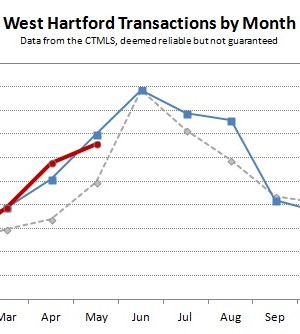

West Hartford continued to see a strong real estate market through the month of May. Below are the four main charts we track to keep in touch with the overall market in town. Closed transactions were down slightly in May compared to May of last year, 66 versus 70. Despite that, 2013 has outperformed 2012 in deal count over the first five months by about 11%, with 238 closings compared to 214 closings. Looking at

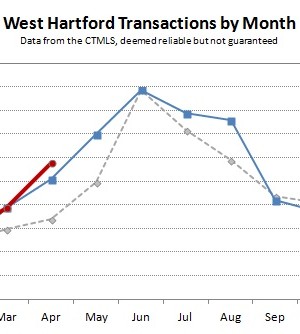

West Hartford has been one of the hottest real estate markets so far this year. Here are a few charts to show where it is as of the middle of the spring season. Data is for single-family homes and comes from the CTMLS, which deemed reliable but not guaranteed. The number of closed sales has at least equaled the 2012 total in every month. Overall, 19% more deals have closed this year compared to the

We’ve written about radon a couple times in the past. Once as an overview to the issue and once when we tested the radon levels in our home. But I don’t think we’ve ever written about the mitigation system itself. A radon mitigation system is just a white PVC tube starting under the foundation and exhausting outside. There is a fan inside the pipe that blows air from out from under the basement. Radon is

We never made any official predictions for the 2012 real estate market. I’m stunned that we didn’t do it because it’s a fun thing to think about, and after analyzing the year-end data we always have thoughts and ideas. We won’t make that mistake again this year … here are our predictions for the coming year. Amy 1. Low inventory in the early months of the year is going to result in more multiple offer