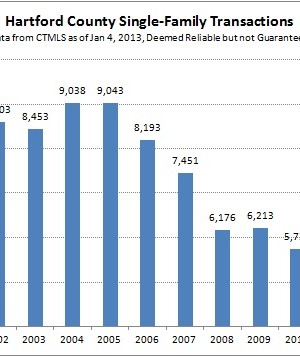

Most of our ongoing analysis of the real estate market is focused on contract data. We like to track contract data because it represents an important milestone, it is more immediate than closings, and it is a strong predictor of closings. But at the end of the year it is also interesting to take a look at the closing numbers since those data points have a meaningful price associated with them. In 2012 the number

Dear Closing Attorney: I hadn’t met you before last Friday, but my client’s mortgage lender recommended that she use you because they have a “closed list” of attorneys they allow buyers to use. I understand this simplifies things for the bank because they can get you to follow certain processes which streamlines their operations. So she went with it. At the closing table you seemed nice enough, making the usual pleasantries and closing jokes as

When you bought your home, did you allow the previous owners to leave items in the basement, garage or attic of the home? When a buyer purchases a property in the Greater Hartford area, it’s supposed to be left in “broom clean condition” by the closing. That means the previous owners shouldn’t leave old paint cans, cleaning products or a host of other things behind. Often you’ll see a seller ask a buyer if it’s

One of the most difficult conversations that I have as a real estate agent is explaining the property tax system in the City of Hartford. Most of the time the subject comes up as I’m touring around with a buyer and trying to cover various home buying subjects as we drive from one property to the next. My client will casually ask about taxes, expecting an answer along the lines of “They’re low/high compared to

Every time a mortgage closes, marketers line up to pitch all sorts of fabulous offers and opportunities to new homeowners. Nearly all arrive via mail so they are, fortunately, easy to sort through and discard. On occasion a company will dispatch their best door-to-door salesman to pay the buyers a visit and congratulate them on their purchase – thankfully they are few and far between. The special offer bounty covers a wide spectrum. Some is