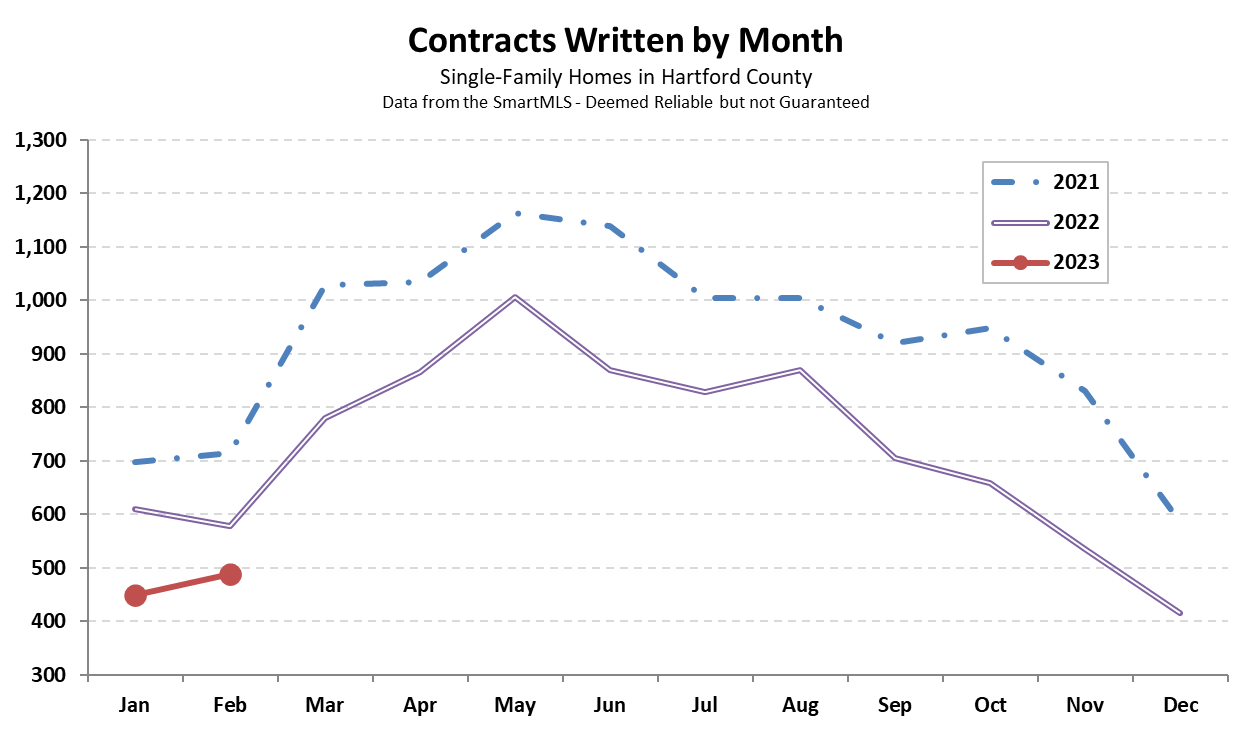

Hartford County finished February with 488 single-family contracts. The total was more than 15% below last February, and comparable to the activity level that we saw in 2010-2014. As recently noted, the bottleneck in the market is on the supply side. There are plenty of buyers, but there are not enough sellers to balance the equation. The number of contracts in a particular month has recently been closely linked to the number of new listings.

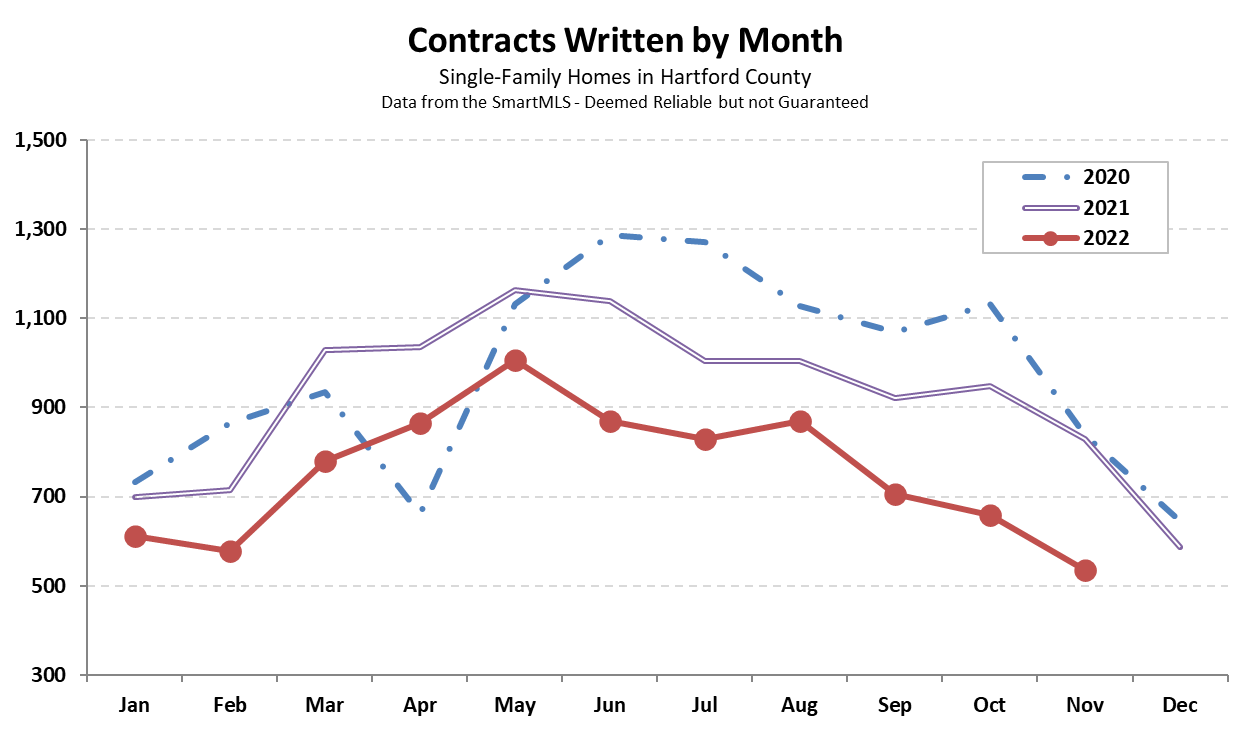

Hartford County finished December, and 2022, with a subdued month in the real estate market. There were 415 contracts signed, about 30% fewer than in December 2021. The year finished 21% behind 2021’s totals. Inventory was the story all year long. It continued to be very low in December, and that is ultimately what limited the number of deals. Buyers who persevered through the holiday months were decisive in bidding quickly and strongly for the

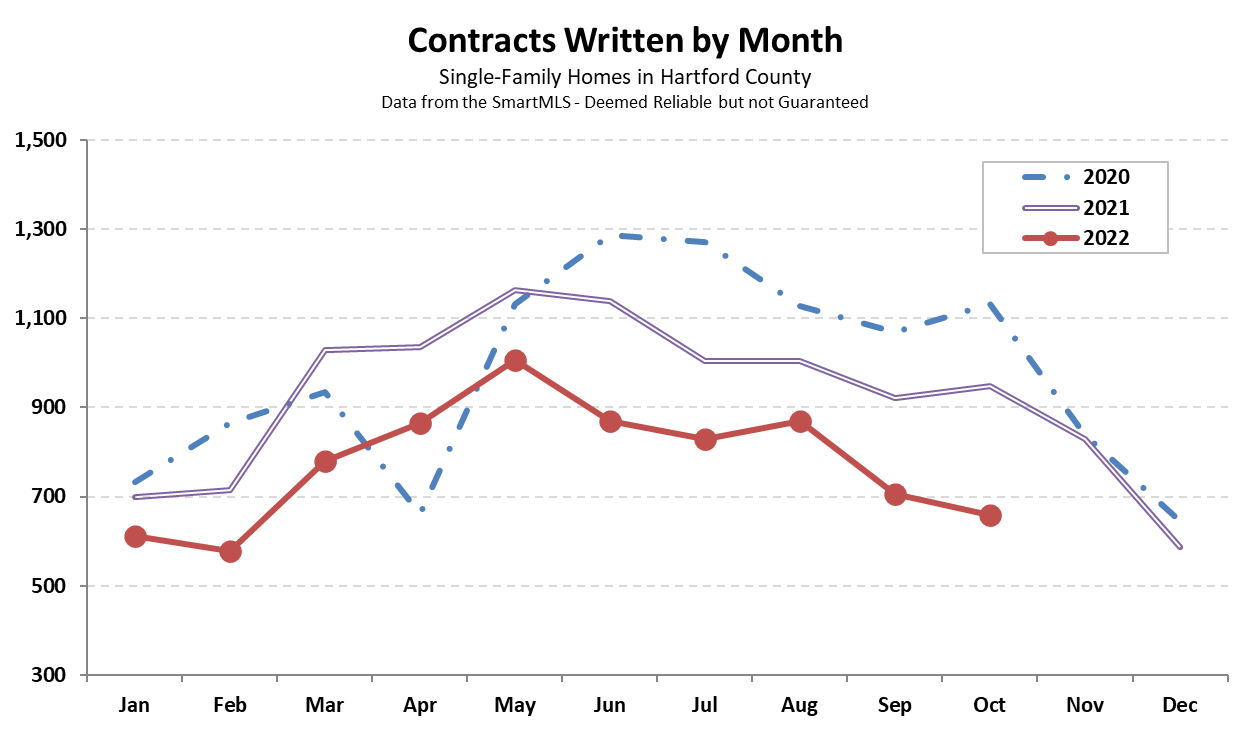

November is often a slow month for the real estate market, and this year was no exception. The County finished the month with 536 single-family contracts, more than 35% fewer than November 2022. On a year-to-date basis the County was 20% behind 2022 totals. The November total deserves a little more context. Yes, it was far below pandemic-era November deal totals. But it was also well above the totals observed during the bottom of the

Noticeably low inventory levels and few new listings led to a quiet October in the Hartford County real estate market, effectively accelerating the winter slowdown by a couple months. The County finished with 658 single-family contracts, which was 30% fewer than the October 2021 total of 948. On a year-to-date basis the County was trailing last year by about 20%. Once again, the total number of contracts for the month closely followed the number of

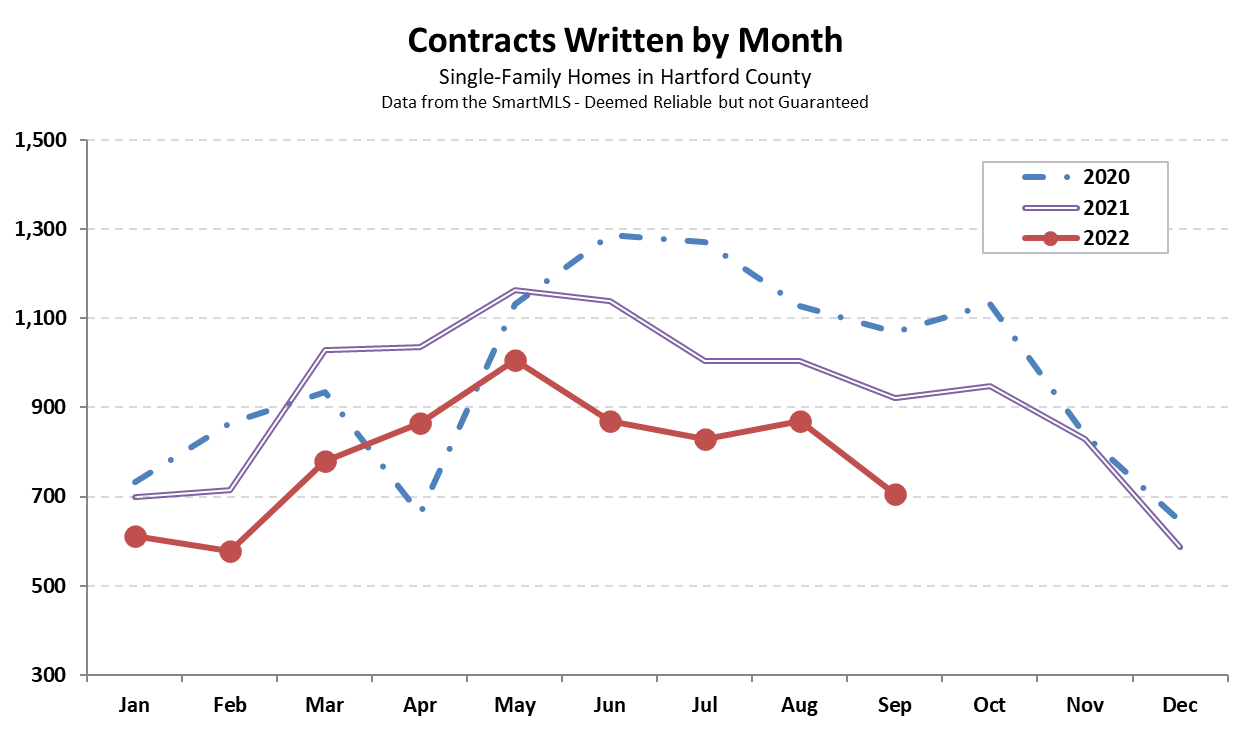

Hartford County finished September with 706 contracts, more than 23% fewer than in September of 2021. The month brought the year-to-date totals down to about 18% behind the number of deals through three quarters in 2021. The number of September listings stepped down just as quickly as the number of contracts. Inventory remained at the 0.9 months level, which means that it is possible buyers slowed down because there were fewer new properties to consider.