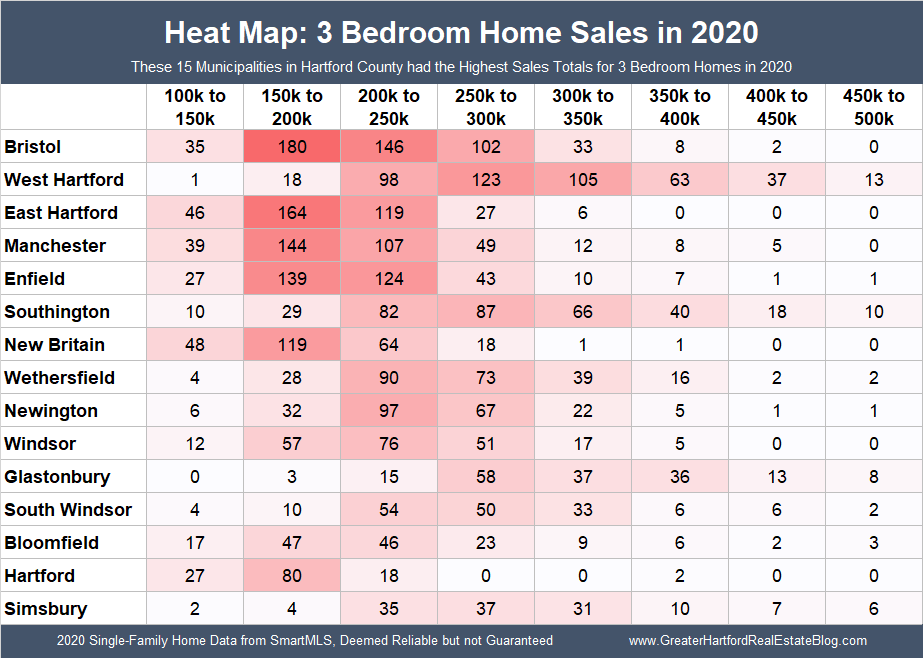

Three bedroom homes are a core part of Greater Hartford’s housing stock. They are popular with buyers, and usually the most active part of the market. The SmartMLS showed that 3 bedroom homes represented more than 53% of the deals in 2020. However, the price of a 3 bedroom home varies from town to town. The chart below shows pricing for 3 bedroom homes in the 15 Hartford County municipalities that had the most 3

I really enjoy gathering and reviewing year-end data from the Greater Hartford real estate market, probably to an unhealthy degree. There is a lot to consider this year, so I broke the analysis into multiple articles. This is Part 3 of the year-end review. The first installment focused on the number of sales, while the second installment looked at pricing. Greater Hartford is divided into many, many towns. These stats look at the 29 municipalities

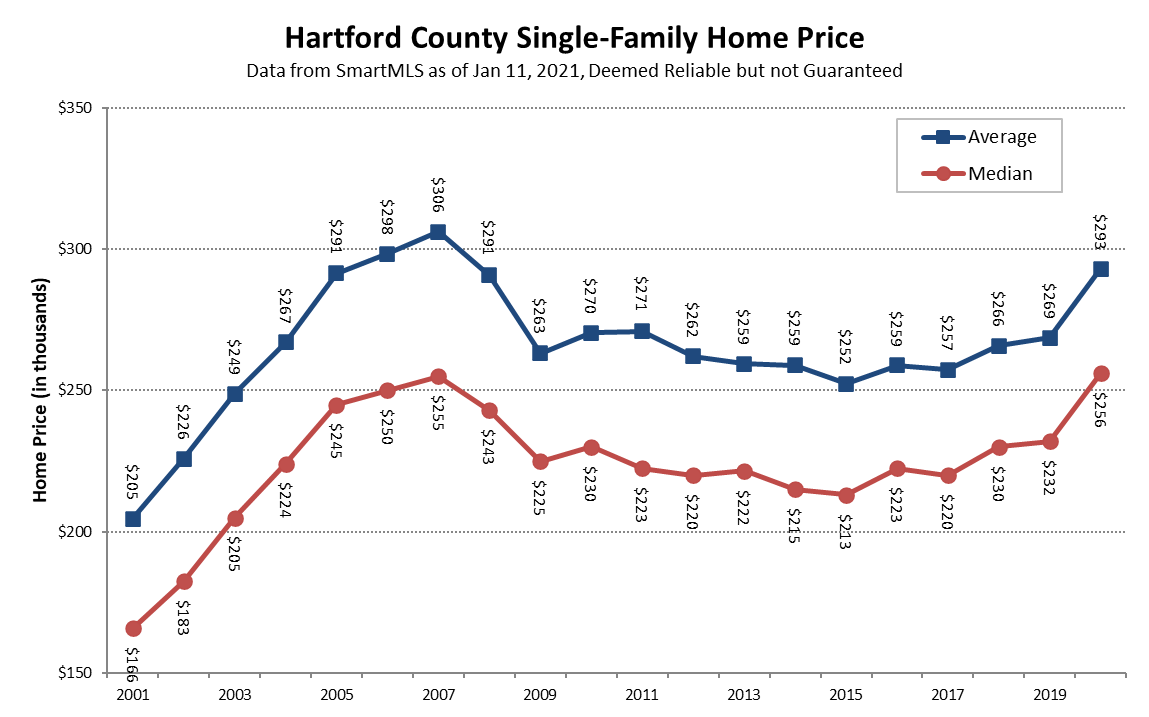

I really enjoy gathering and reviewing year-end data from the Greater Hartford real estate market, probably to an unhealthy degree. There is a lot to consider this year, so I broke the analysis into multiple articles. This is Part 2 of the year-end review … the first installment focused on the number of sales. The sharp increase in demand for Hartford County single-family homes during 2020, combined with a decrease in supply of available homes,

Home buyers naturally want to get the best deal possible on their purchase. But in this market they have to balance that instinct against their desire to win one of the relatively few available properties. Buyers have to BUY the home they want. Sellers are not going to give them the home. And a bidder thinking that they’d be okay taking the home – but only at their price – is unlikely to get anything

Opportunities often arise when a market is out of balance. Right now the real estate markets are severely out of balance with far more demand for housing than supply. Part of our job as real estate advisers to highlight and explain these opportunities. Sellers currently have the upper hand in the market, and therefore the opportunity. However, slight variations in the current environment mean that this is a more valuable opportunity for some owners than