We are available for private consultations, to answer your questions about buying a home or anything else related to real estate, on a variety of video conferencing platforms. I lead with that because I’ve noticed an explosion of virtual buyer seminars advertised since video conferences became the norm. Buyer seminars happened before Zoom, of course, so it’s not like they are totally new. However, they are much more efficient to organize virtually. And the big

The Fair Isaac Corporation rates personal creditworthiness of basically everyone using its FICO Score model. Our individual FICO Score factors into the pricing we receive on all of our borrowing, and most of the financial services we purchase. It is a critical driver in mortgage loan availability and interest rates for home buyers. In late January, Fair Isaac announced an update to their FICO Score model. The new credit scoring methodology will be available to

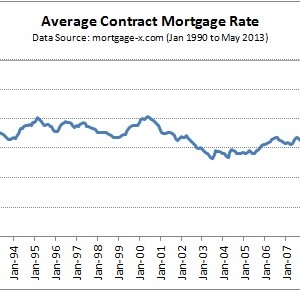

As those actively looking for a home can tell you, mortgage rates have risen sharply in the past two months. The chart to the right shows the average rate for a 30-year fixed-rate loan since the beginning of the year. The chart is from the Bankrate.com site. From January through the beginning of May, mortgage interest rates bounced around the 3.5% level. But then, over the course of a little more than a month they

How strong is the bid we just submitted for that property you love? Are you going to get the house? Sellers are receiving multiple offers on a regular occasion this spring. Buyers are lined up, anxious to buy a home, and willing to submit offers on homes as soon as they hit the market. In many cases buyers know they need to write up their best offer immediately – there may not be an opportunity

We never made any official predictions for the 2012 real estate market. I’m stunned that we didn’t do it because it’s a fun thing to think about, and after analyzing the year-end data we always have thoughts and ideas. We won’t make that mistake again this year … here are our predictions for the coming year. Amy 1. Low inventory in the early months of the year is going to result in more multiple offer