There is an active market for leads in real estate, though the economics are generally hidden from the public. I thought it would be a good idea to shine a light on this corner of the industry so that you can understand how it all works. Real Estate agents build their business based on three main types of leads; Direct, Paid, and Contingent. The differences between these lead types matter because the economics vary for

I’m excited to share a project that has been in the works for a while. It’s ready to take the next step, and needs your help. MeetingInfo.org is a web service that organizes information about public meetings. It’s designed to help meeting organizers connect with their constituents by publishing their meeting information online. As a quick example, the site is perfect for municipalities, with their dozens of Councils, Boards, and Committees. The City of Hartford

The old saying that a rising tide lifts all boats takes on new meaning now that we know that sea level is actually rising in addition to the tide. Regional differences in the impact of sea level change will prevent everyone from sharing the same outcome as the water advances. Many areas will struggle with higher tides, while others will benefit. Hartford, as an inland metropolitan region, has an advantage over our coastal neighbors. Articles

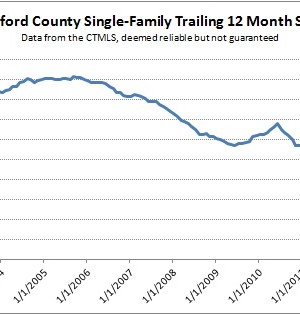

While reviewing real estate transaction data, the following chart caught our attention. It shows the number of single-family home sales that have closed in Hartford County over rolling 12 month periods. Said another way, each data point is the number of total sales over the previous 12 months. Note that this chart has nothing to do with values, only transaction counts. The line in the chart bounces around in the 8,000 deals-per-year range from the

We found Portsmouth to be a very interesting place. And as residents of an area trying to build the type of vibrancy that they seemed to already have, it was difficult not to compare and contrast Portsmouth with the Hartford area. For background, the City of Portsmouth proper is only 15.6 square miles and has a population of about 21,000. This is about the same geographic size as our municipalities, as the City of Hartford