Don’t miss this thoughtfully updated, well maintained Cape in West Hartford’s popular Elmwood neighborhood. First, enter into the sunny living room. The hardwood floors and wood burning fireplace welcome you home. This opens to the remodeled kitchen with stone counters, plenty of cabinet space, stainless appliances, and an eat-in area. Down the hall you’ll find a full bathroom and two of the home’s four bedrooms. Upstairs, there are two more nicely sized bedrooms. You’ll appreciate

You’ll love this thoughtfully updated 4-bedroom, 2-bathroom Cape, located on a quiet cul-de-sac. The main level features a formal living room with wood burning fireplace. This leads to the dining room and updated kitchen. Enjoy plenty of cabinet space, a pantry, tile flooring, leathered granite counters, stainless steel appliances, and a separate breakfast room. An oversized primary bedroom and renovated full bathroom complete the first floor. Upstairs are three additional bedrooms, each with hardwood floors,

This 6-unit brick apartment building is a great investment opportunity in Hartford’s Clay Arsenal neighborhood. Each unit is spacious with five rooms- a kitchen, living room/dining room, two bedrooms, bonus room, and full bathroom. All of the windows have been replaced. The property has public water and sewer, as well as natural gas. The interior of the property will need significant rehab and a trash out, as it was previously vandalized. All utilities are turned

Some buyers set out to find a Complete and Total Disaster when they are shopping for a new home. Is that what you’re looking for? Because we come across them periodically and can point you in the right direction. Most buyers don’t want to do quite that much work on their new home, so they stick to the upper half of the quality chart shown above. The real challenge is knowing whether the home you

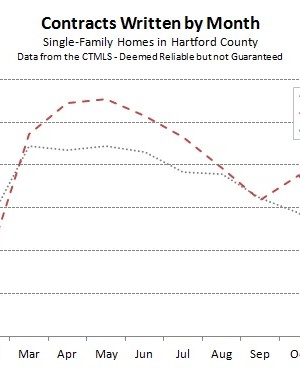

The Hartford County single-family home market began 2014 with 519 contracts in January. The total was more than 4% lower than January of last year, though still higher than any other year since our data began in 2009. January was the longest cold stretch that we can remember in Greater Hartford. There have been brief deep freezes, but our experience in the area is that the temperature rarely falls below 20 degrees for long. This