The practice of buying and quickly reselling real estate is well established. It generally goes by the name of “flipping.” There are different business models under the broad umbrella of flipping, with different risk and return profiles. At one end of the spectrum Wholesalers try to buy super cheap by finding private deals. At the other end of the spectrum Renovators focus on adding value to a property through construction. Despite the easy profits shown

I saw a few interesting real estate articles recently that capture some of the trends in the California market. A company with locations in Los Angeles and San Francisco is renting out individual bunks in a home for $1,200 per month. You get a bed, and a shelf, and a wall mounted TV. There might also be a curtain built it. Guests are not allowed into the building – only residents. Google has partnered with

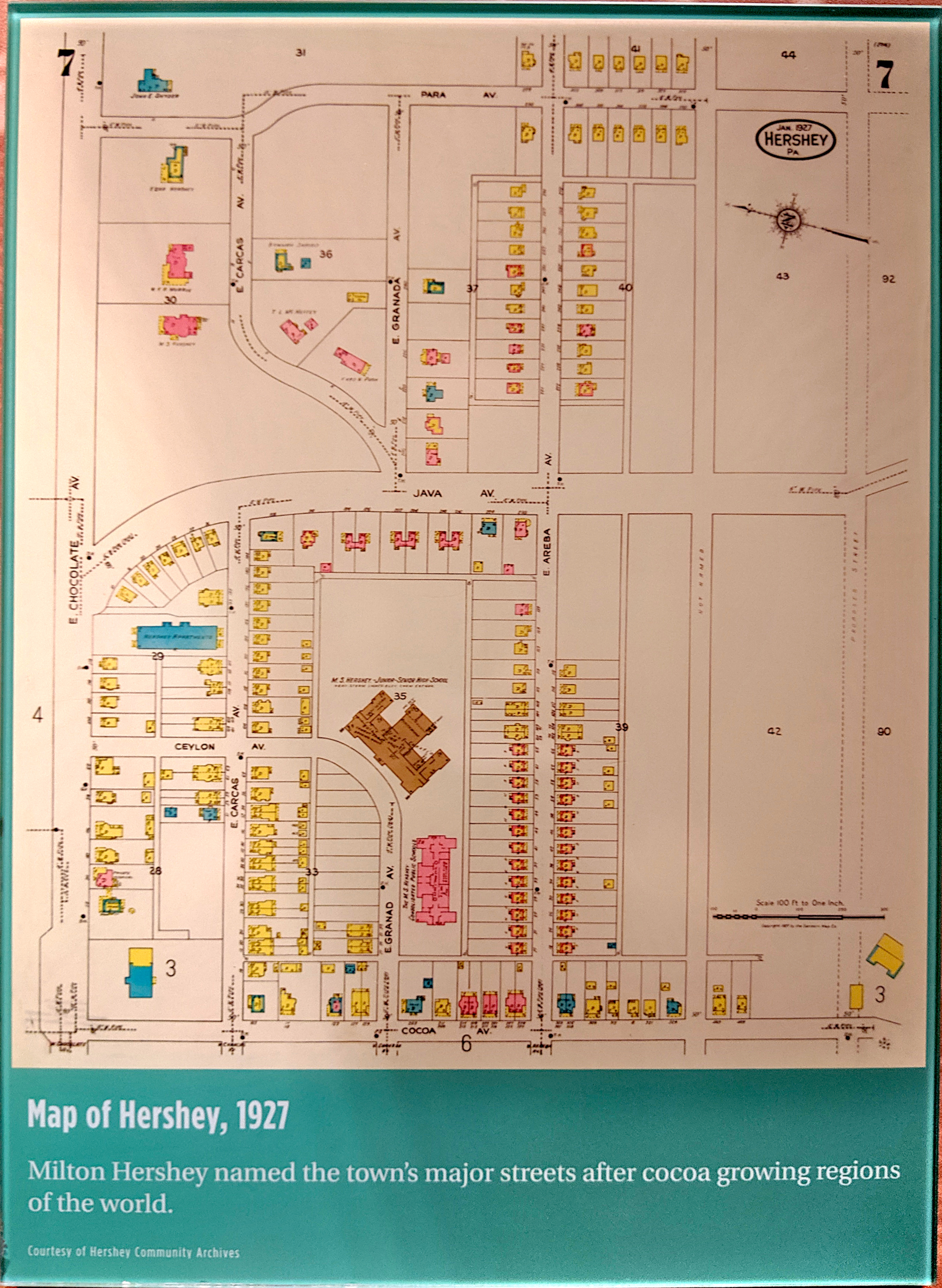

Our non-work adventures recently took us to Hershey, Pennsylvania for sightseeing. It turns out that the town was planned by the chocolate mogul himself to be a form of “company town” like he had seen in other parts of the world. His spin on the idea was to try to be nice to his workers by encouraging homeownership, selling homes at affordable prices, and providing easy payment plans to finance the purchases. He also encouraged

It’s always fun to survey different markets to compare prices. Today we have three $1,600/month rentals for your consideration: Option 1 is a totally updated 2 bedroom at 33 Charter Oak Place in Downtown Hartford. Option 2 is a spacious 3 bedroom in a great location at 151 Maplewood Avenue in West Hartford. Option 3 is … whatever this is in NYC: $1,600 per month/studio Chelsea, NYC pic.twitter.com/HoY11iE8Yq — J (@AmericaCanceled) February 9, 2019 Clearly

A finance guy paid $238 million for a large apartment at the top of a building overlooking Central Park. The CTMLS says that the total cost of the 687 residential properties (single-units, multi-units, and condos) that sold in Hartford in all of 2018 was $109.3 million. This comes out to about $159,153 per property. West Hartford, which has the most active residential market in this area and strong prices, was able to top that one