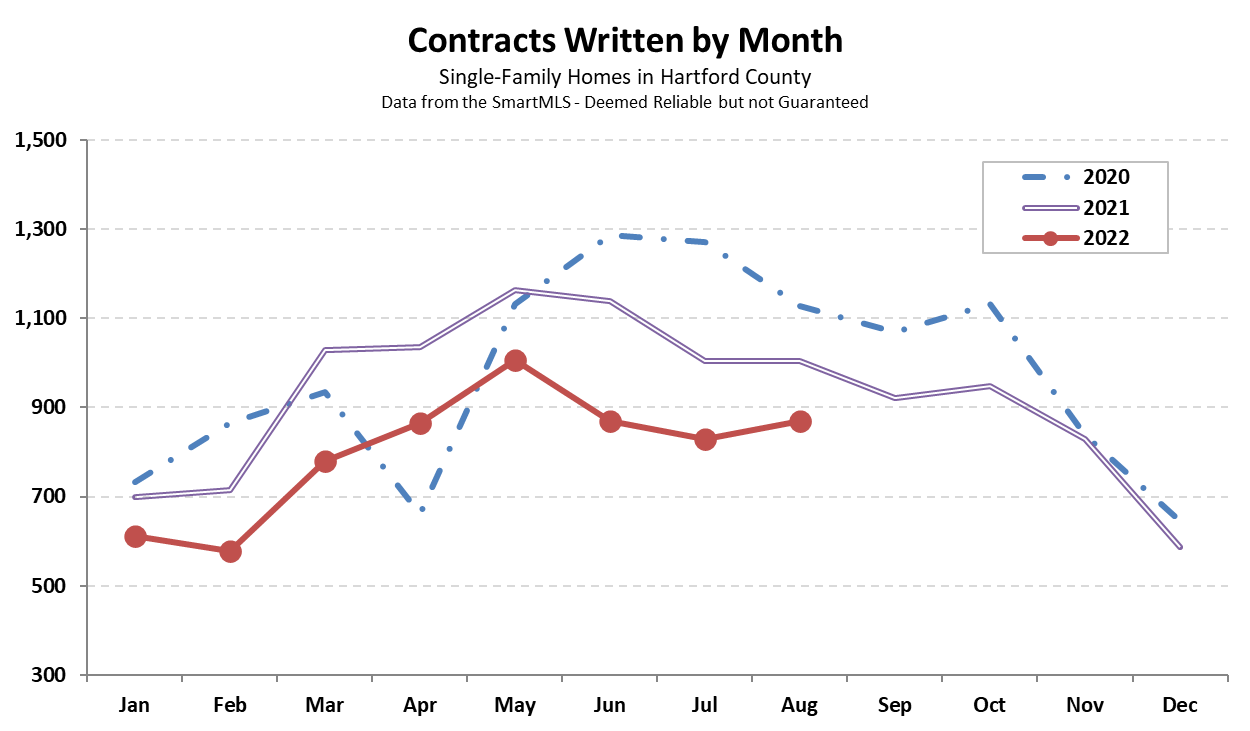

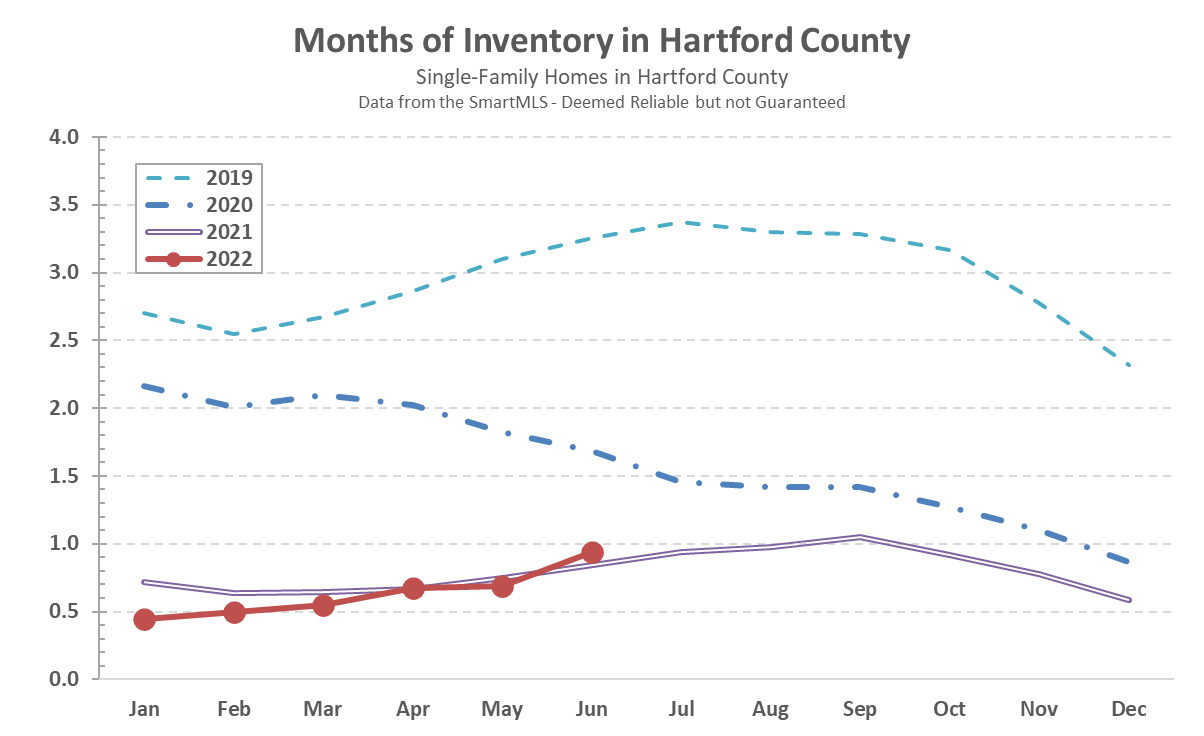

Hartford County closed the summer with an uptick in the number of contract. August finished with 870 deals, a slight increase over July but still below the August 2021 total. Overall the County was over 17% behind 2021 on a year-to-date basis. Inventory levels moved downward for the first time since January. We continued to hover around one month of homes available, a strong seller’s market, and the long-term trend of fewer options at lower

Hartford County finished June with 869 single-family contracts. It was a 23% decline from the June 2021 total, leaving the County 18% behind 2021 through the first half. The 869 contract, when seen as a measure of buyer activity, is a meaningful retreat. June is one of the busier months in the seasonal real estate market, with contract totals often near the peak. June 2022 showed a meaningful fall-off from the May peak, and was

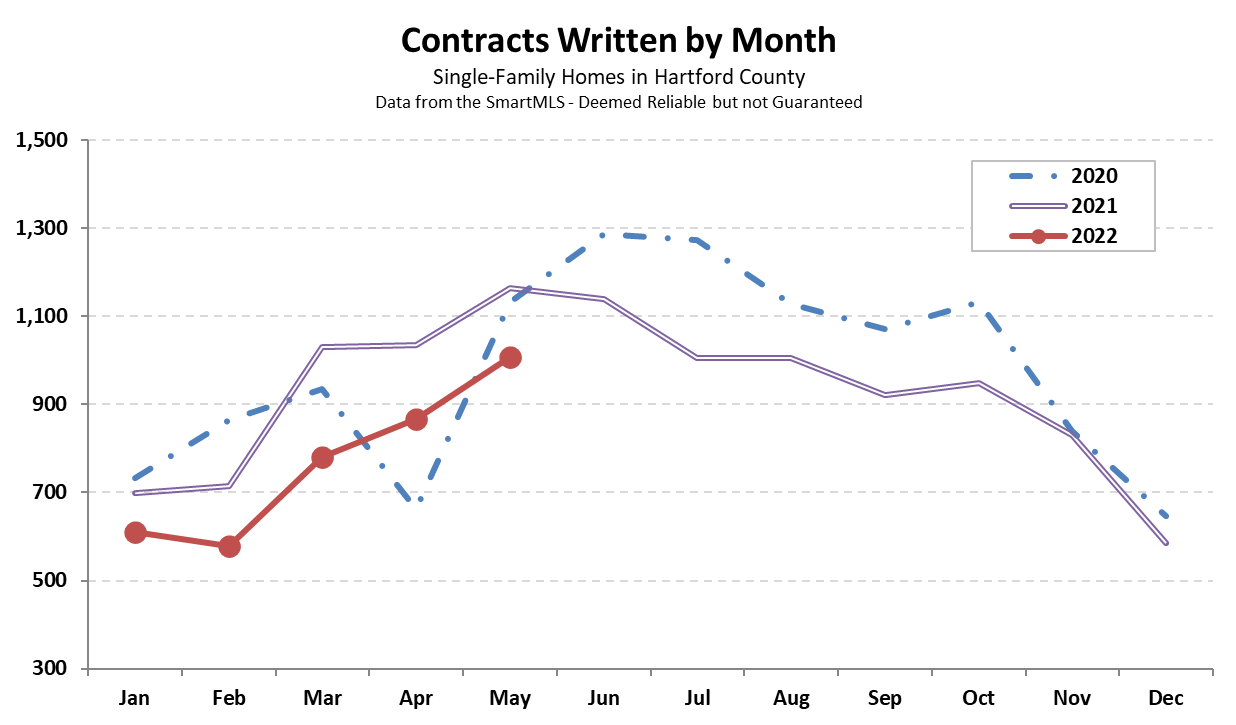

During May, buyers and sellers balanced each other out in Hartford County’s long-running struggle with inventory. New deals totaled 1,007, while new listings totaled 1,035. Both were solid numbers that showed both sides were still engaged in the market. Comparing 2022 to prior years, May finished with about 13% fewer contracts than May 2021. On a year-to-date basis 2022 trailed 2021 by about 17% through the end of May. Inventory remained stable compared to last

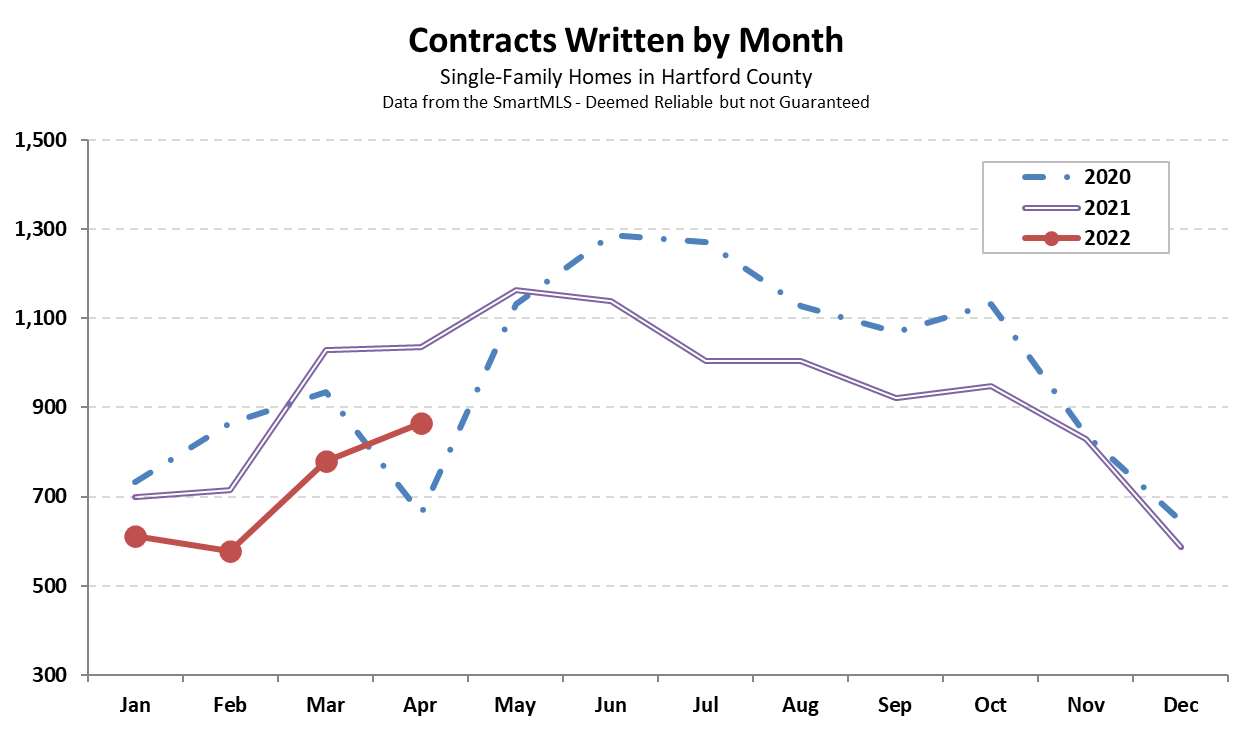

All Hartford County single-family metrics improved during the month of April. The number of contracts stepped upwards to 866, a strong increase over March 2022, but still about 16% behind the April 2021 total. The market finished the month about 18% behind 2021 on a year-to-date basis. New listings topped the 1,000 level for the first month since the tail end of last summer. Because contracts remained below new listings, the overall inventory of available

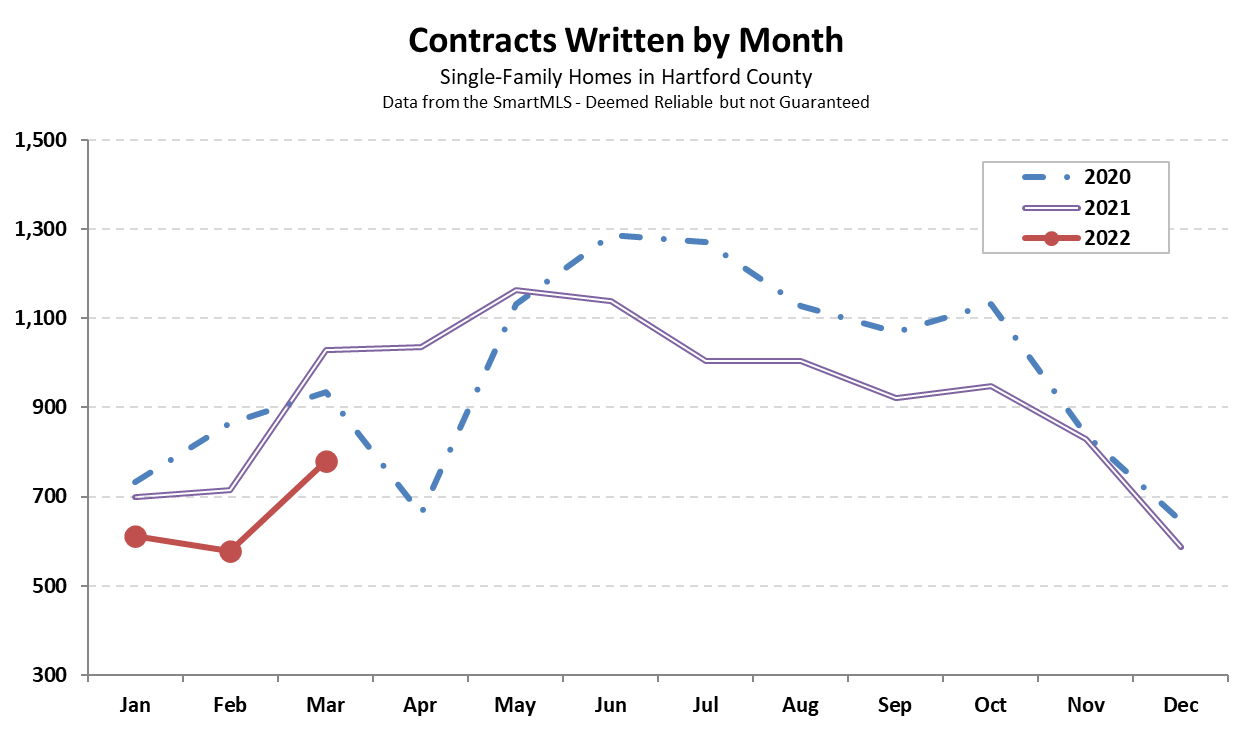

Hartford County finished March with 780 single-family contracts signed. The total was about 24% fewer the March 2021 tally, putting 2022 about 19% behind 2021 on a year-to-date basis. We’ve written at length about low inventory. A new data point illustrating inventory challenges is that listings in Q1 were down more than 13% from 2021. Listings in Q1 2021 were down 20% from 2020. Combining those two numbers, there were 31% fewer listings in Q1