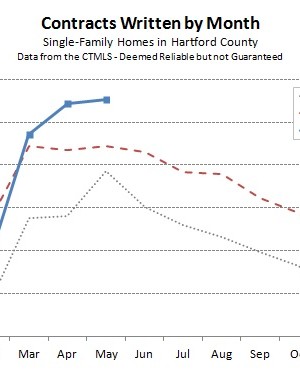

Hartford County single-family contracts edged up in May to 855 deals, a 1% increase over April of this year. More impressively, the month was more that 14% more active than May of last year. The active season extended later into the spring before the deal count plateaued. Through May, the market is more than 7% ahead of the 2012 market in terms of deal count. Drilling down into the individual towns, the numbers bounce all

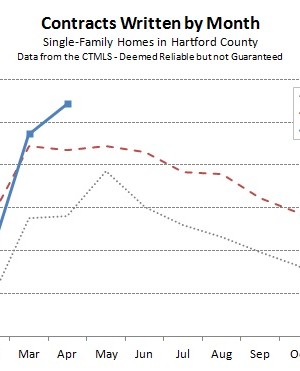

The Hartford County single-family housing market continued its strong spring. Overall, buyers and sellers agreed to 845 deals during the month, which is nearly 15% higher than April of 2012. The year-to-date number of contracts is more than 5% ahead of where it was at this point last year. Strong April performance helps support our view that the February result was an aberration. Both March and April finished with higher contract totals than any individual

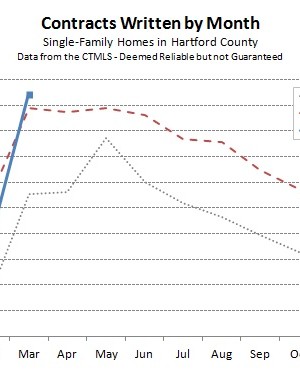

February was slow. March bounced back to above the 2012 trend with 773 deals coming together. This is about 4% over the March 2012 result. Since the market continues to be very active, we still believe that February was an aberration and should not be interpreted as weakness in the single-family real estate market in Hartford County. Buyers in many towns, and at a variety of price points, are frustrated by the low number of

How strong is the bid we just submitted for that property you love? Are you going to get the house? Sellers are receiving multiple offers on a regular occasion this spring. Buyers are lined up, anxious to buy a home, and willing to submit offers on homes as soon as they hit the market. In many cases buyers know they need to write up their best offer immediately – there may not be an opportunity

February was dramatic and interesting; the market statistics brought something new and different to think about and interpret. There were 489 Hartford County single-family contracts, a 13% decrease from February of 2012 and a 10% decrease from January of 2013. As the month progressed, we felt that the market had noticeably slowed from the January pace. But it’s very difficult to know how much of what we see is specific to our current set of