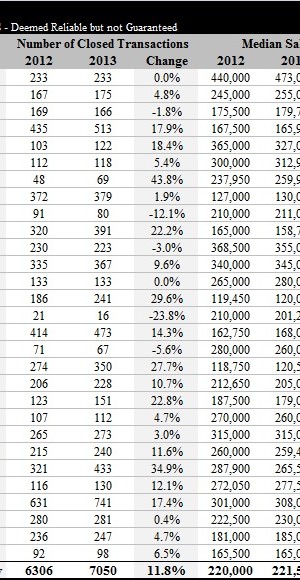

Last week we published some charts showing the direction of the overall single-family market in Hartford County for 2013. The quick summary was that sales activity has been increasing nicely for two years, but median prices have been stuck in a protracted valley. The data tells a variety of different stories when we zoom in to the individual towns. Before we get there though, a quick disclaimer. It’s difficult to take too strong a position

West Hartford finished August 2013 with 84 single-family closings, up from 76 in August of 2012. Overall the town is about 12% ahead of 2012 in terms of transactions. The most active price bands are showing an increase in activity over the past 12 months. Homes priced at the upper end of the market are in line with the previous year. However, at the lower end of the market there has been a 13% decrease

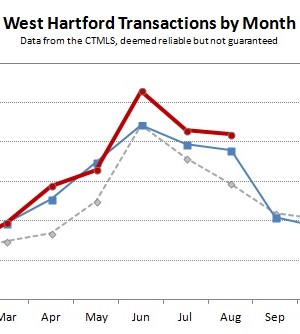

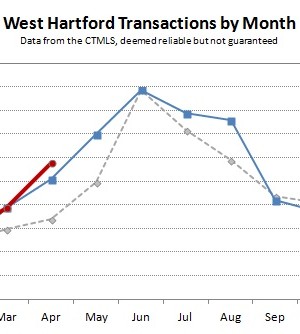

West Hartford has been one of the hottest real estate markets so far this year. Here are a few charts to show where it is as of the middle of the spring season. Data is for single-family homes and comes from the CTMLS, which deemed reliable but not guaranteed. The number of closed sales has at least equaled the 2012 total in every month. Overall, 19% more deals have closed this year compared to the

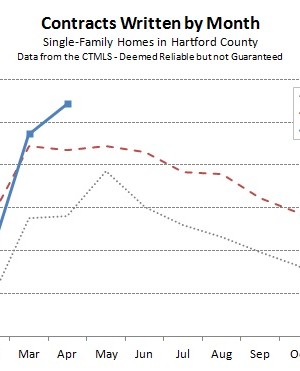

The Hartford County single-family housing market continued its strong spring. Overall, buyers and sellers agreed to 845 deals during the month, which is nearly 15% higher than April of 2012. The year-to-date number of contracts is more than 5% ahead of where it was at this point last year. Strong April performance helps support our view that the February result was an aberration. Both March and April finished with higher contract totals than any individual

February was dramatic and interesting; the market statistics brought something new and different to think about and interpret. There were 489 Hartford County single-family contracts, a 13% decrease from February of 2012 and a 10% decrease from January of 2013. As the month progressed, we felt that the market had noticeably slowed from the January pace. But it’s very difficult to know how much of what we see is specific to our current set of