This quaint 2-bedroom, 1.5-bathroom Colonial is located on a quiet and convenient Newington street. You’re close to popular shops and restaurants in the Center and on the Turnpike, the town library, Mill Pond Park, and the Eddy Farmstand. Inside, an enclosed porch leads to the formal living room. A dining room with built-in hutch connects to the kitchen and first floor powder room. Upstairs you’ll find a primary bedroom with multiple closets, second bedroom, and

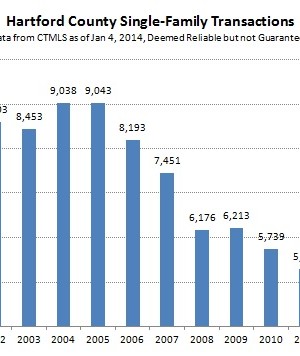

Most of the year we avoid looking at prices when we analyze market statistics. Considering only a month’s (or even quarter’s) worth of data is risky because the sample size is too small, while making a more sophisticated model to account for the small sample size is beyond our abilities. However we are comfortable looking at a full year of data, and now that the calendar has turned over to 2014 we can look back

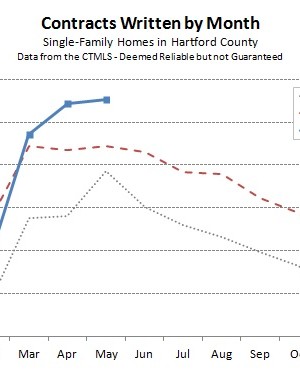

Hartford County single-family contracts edged up in May to 855 deals, a 1% increase over April of this year. More impressively, the month was more that 14% more active than May of last year. The active season extended later into the spring before the deal count plateaued. Through May, the market is more than 7% ahead of the 2012 market in terms of deal count. Drilling down into the individual towns, the numbers bounce all

This move-in ready townhouse at Crown Ridge is convenient to shopping, restaurants and highway access, while still privately located. You’ll enter the condo at ground level into a tiled foyer with coat closet. The attached 1-car garage connects to this space, as well as a large unfinished area, perfect for storage. Upstairs is the main living area. A formal living room has a wood burning fireplace and French doors out to a deck. The living

February was dramatic and interesting; the market statistics brought something new and different to think about and interpret. There were 489 Hartford County single-family contracts, a 13% decrease from February of 2012 and a 10% decrease from January of 2013. As the month progressed, we felt that the market had noticeably slowed from the January pace. But it’s very difficult to know how much of what we see is specific to our current set of