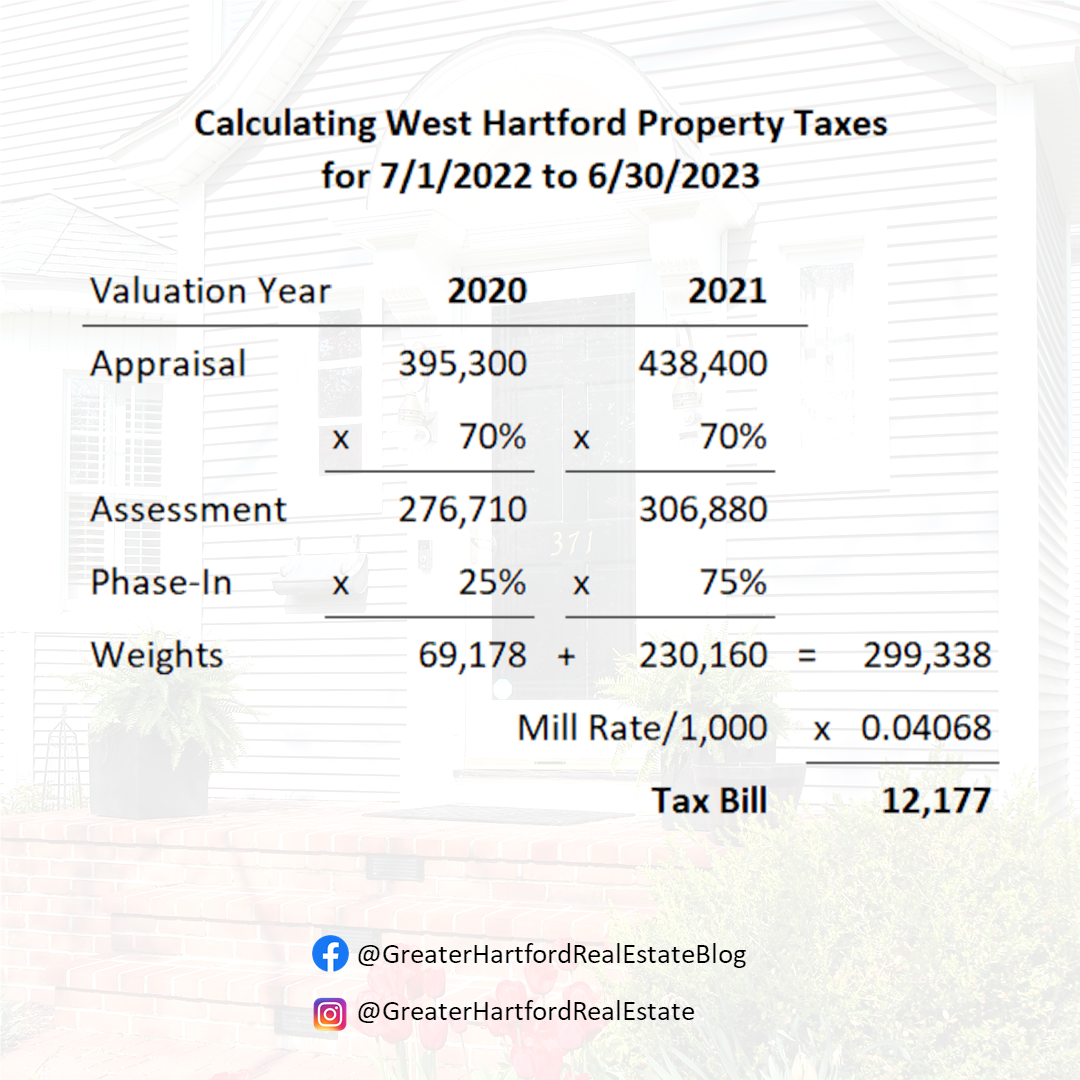

West Hartford’s adopted budget for the fiscal year running from 7/1/2022 to 6/30/2023 includes a phase-in of the recent property revaluation. The phase-in adds a degree of difficulty to calculating the property tax bill of each individual parcel. The State of Connecticut requires municipalities to do revaluations every 5 years. The goal is to ensure that property owners contribute to the expenses of the town proportionally based on the fair market value of their property.

The 2021 Hartford Revaluation was delayed compared to the typical revaluation timeline. In late December we published an update on the revised schedule, and this update details the final steps. Yesterday we got an update letter from the City of Hartford Tax Assessor’s office. Every property owner in the City should have received one, as it updated the assigned revaluation 2021 market values after completing the informal challenge process with the contractor. If you had

We spoke with the City of Hartford Assessor earlier today to get an update on the timeline for the City’s 2021 Revaluation. The current target for distributing assigned market values to all the property owners in the City is late January. The Assessor’s staff, and the contractors helping with the revaluation, are taking extra time to be sure that they feel totally confident in the values before sending them out. Even though this approach creates

In June of 2013 the City established a Task Force “for the purpose of examining and analyzing Hartford’s property tax system, and making recommendations for State legislation to rectify imbalances resulting from the system.” We follow the City’s property tax system closely, and the Task Force’s recently released final report makes this a good opportunity to quickly review Hartford’s current tax situation, analyze the recommendations of the Task Force and share our thoughts. Hartford’s property

Speculating that the mortgage interest tax deduction might go away is currently quite popular. News sites all across the internet have taken various angles on what it might mean to individual homeowners and the real estate markets in general. Most articles argue that eliminating this tax break will cause home values to decrease. The National Association of Realtors is frequently quoted as estimating that home prices would fall by 15% nationally and more in areas