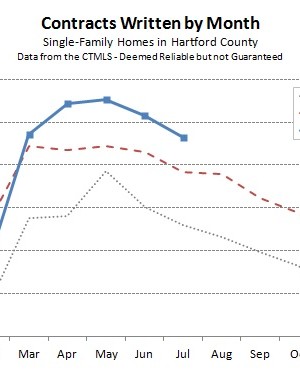

There were 766 single-family contracts written in July in Hartford County. This is an 11% increase over July in 2012, and about a 6% decrease from last month. One important point to note is that we have revised the June contract count upwards by a significant number – see the original June post here. While working on the July numbers we found a spreadsheet error that had caused 67 contracts to be omitted from the

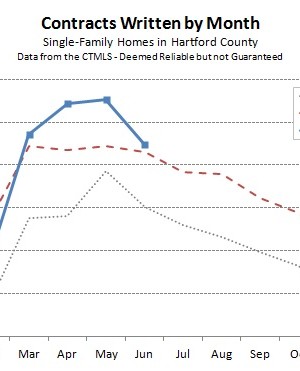

Seven hundred and forty-nine single-family homes went under contract in Hartford County during the month of June. As the chart below shows, this was slightly ahead of last year, though a clear decline from the peak of the market in April and May. The summer market begins at different times each year. Last year the spring market momentum carried through August with only a modest fall off in monthly deal totals. This year June is

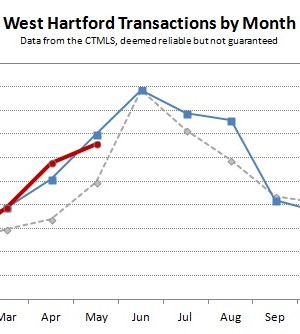

West Hartford continued to see a strong real estate market through the month of May. Below are the four main charts we track to keep in touch with the overall market in town. Closed transactions were down slightly in May compared to May of last year, 66 versus 70. Despite that, 2013 has outperformed 2012 in deal count over the first five months by about 11%, with 238 closings compared to 214 closings. Looking at

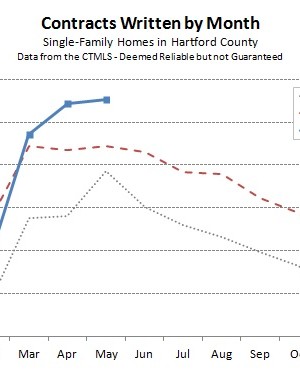

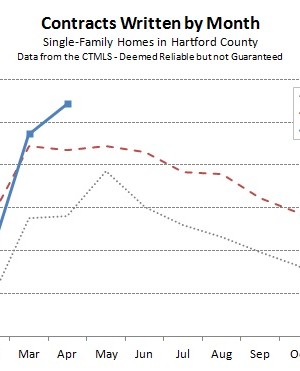

Hartford County single-family contracts edged up in May to 855 deals, a 1% increase over April of this year. More impressively, the month was more that 14% more active than May of last year. The active season extended later into the spring before the deal count plateaued. Through May, the market is more than 7% ahead of the 2012 market in terms of deal count. Drilling down into the individual towns, the numbers bounce all

The Hartford County single-family housing market continued its strong spring. Overall, buyers and sellers agreed to 845 deals during the month, which is nearly 15% higher than April of 2012. The year-to-date number of contracts is more than 5% ahead of where it was at this point last year. Strong April performance helps support our view that the February result was an aberration. Both March and April finished with higher contract totals than any individual