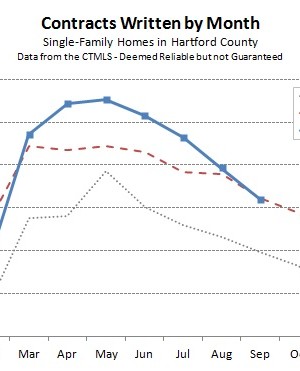

September contract data for Hartford County single-family home sales showed a decrease in activity on both a month-over-month basis and a year-over-year basis. The final count was 620 contracts for September, which was slightly behind the 625 from September 2012. We were very surprised by how the month developed. After a flurry of activity at the end of August and the beginning of September, we were expecting a strong month and a step up in

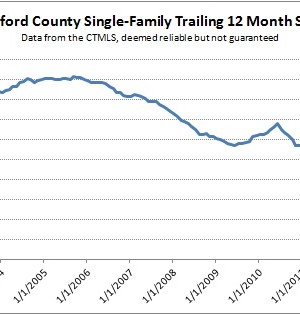

While reviewing real estate transaction data, the following chart caught our attention. It shows the number of single-family home sales that have closed in Hartford County over rolling 12 month periods. Said another way, each data point is the number of total sales over the previous 12 months. Note that this chart has nothing to do with values, only transaction counts. The line in the chart bounces around in the 8,000 deals-per-year range from the

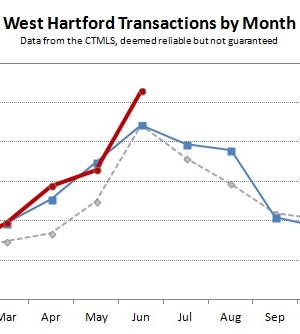

The West Hartford single-family real estate market continues to outperform 2012 in a year-over-year comparison. Closings in June jumped up to 106, which was the best individual month for the town since June 2006 (with 114 closings). Many buyers like to close on their new homes in the summer months. June is usually the peak for closings, with July and August showing modest declines from a June peak depending on the overall strength of the

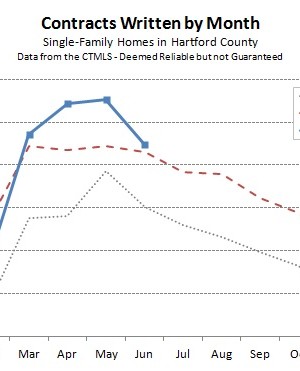

Seven hundred and forty-nine single-family homes went under contract in Hartford County during the month of June. As the chart below shows, this was slightly ahead of last year, though a clear decline from the peak of the market in April and May. The summer market begins at different times each year. Last year the spring market momentum carried through August with only a modest fall off in monthly deal totals. This year June is

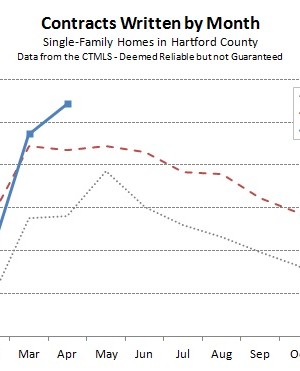

The Hartford County single-family housing market continued its strong spring. Overall, buyers and sellers agreed to 845 deals during the month, which is nearly 15% higher than April of 2012. The year-to-date number of contracts is more than 5% ahead of where it was at this point last year. Strong April performance helps support our view that the February result was an aberration. Both March and April finished with higher contract totals than any individual