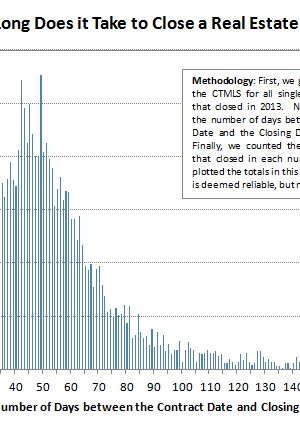

The amount of time between the contract date and the closing varies greatly – every situation is a little different. However, after looking at all of the single-family deals that closed in Hartford County in 2013 we can see some trends. The peak of the curve is between 35 and 55 days. This is the range that we usually see with our clients. It allows the buyer enough time to secure a mortgage, and the

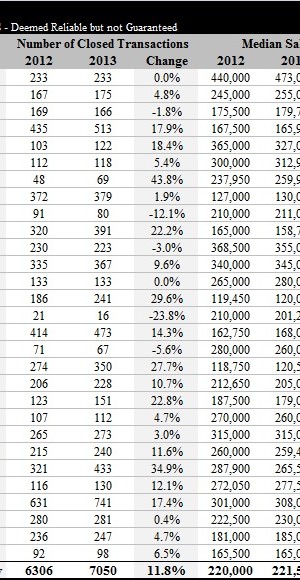

Last week we published some charts showing the direction of the overall single-family market in Hartford County for 2013. The quick summary was that sales activity has been increasing nicely for two years, but median prices have been stuck in a protracted valley. The data tells a variety of different stories when we zoom in to the individual towns. Before we get there though, a quick disclaimer. It’s difficult to take too strong a position

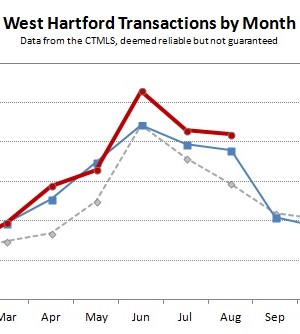

The West Hartford real estate market finished September 2013 with 52 closings, which was nearly 24% more than the total from September of last year. For the whole year, the 2013 transaction total is about 13% ahead of 2012. There have not been any major changes in the stats since August. The distribution of closed deals has been pretty consistent over the different price bands. The number of properties under contract has fallen slightly from

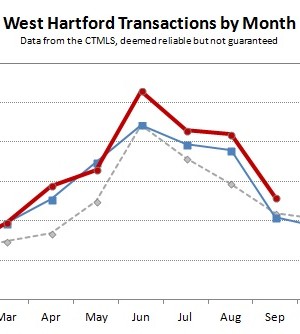

West Hartford finished August 2013 with 84 single-family closings, up from 76 in August of 2012. Overall the town is about 12% ahead of 2012 in terms of transactions. The most active price bands are showing an increase in activity over the past 12 months. Homes priced at the upper end of the market are in line with the previous year. However, at the lower end of the market there has been a 13% decrease

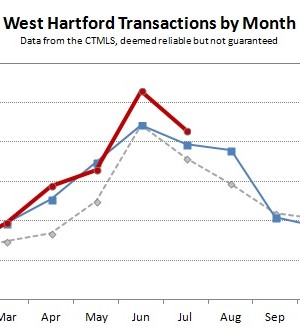

July was an active month in the West Hartford single-family real estate market, but not quite as exciting as June. There were 86 closings in July, which was modestly above the 2012 count, and on a year-to-date basis we are about 12% ahead of 2012 in the total number of closed deals. The statistics can shift a lot over the summer months. Buyers that put properties under contract in the spring close on those deals